Historical

The term “rare earths” (RE) originated in the late 18th and early 19th centuries when these elements were first discovered centuries ago. Despite the name, they are neither rare nor rare earth elements. However, at the time, they were challenging to separate and were only found in relatively rare deposits. In fact, rare earth elements are relatively abundant in the earth’s crust, but they are rarely found in a concentrated and economically valuable form compared to ores of other metals.

")

How Do Rare Earth Elements Impact the Energy Transition?

The overarching goal of the Paris Agreement is to limit the rise in global average temperature to no more than 2 °C above pre-industrial levels, while pursuing efforts to cap warming at 1.5 °C.¹⁶

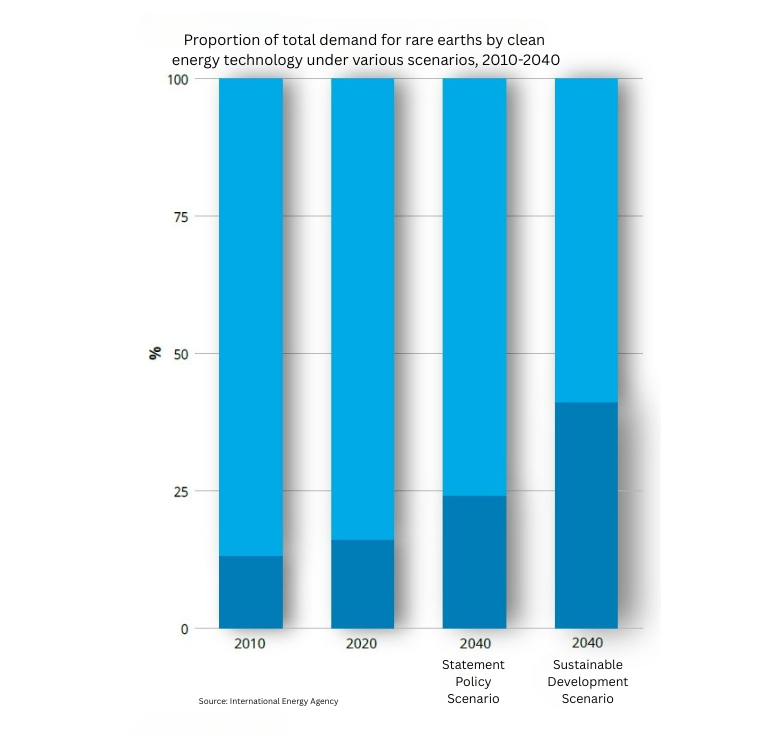

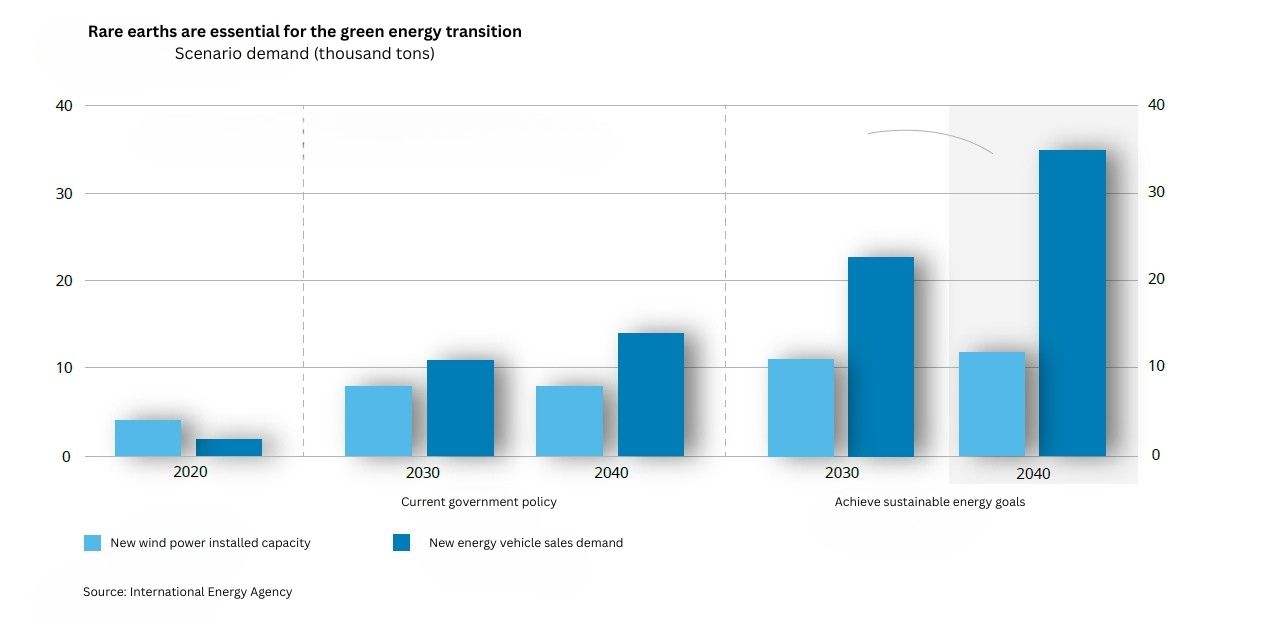

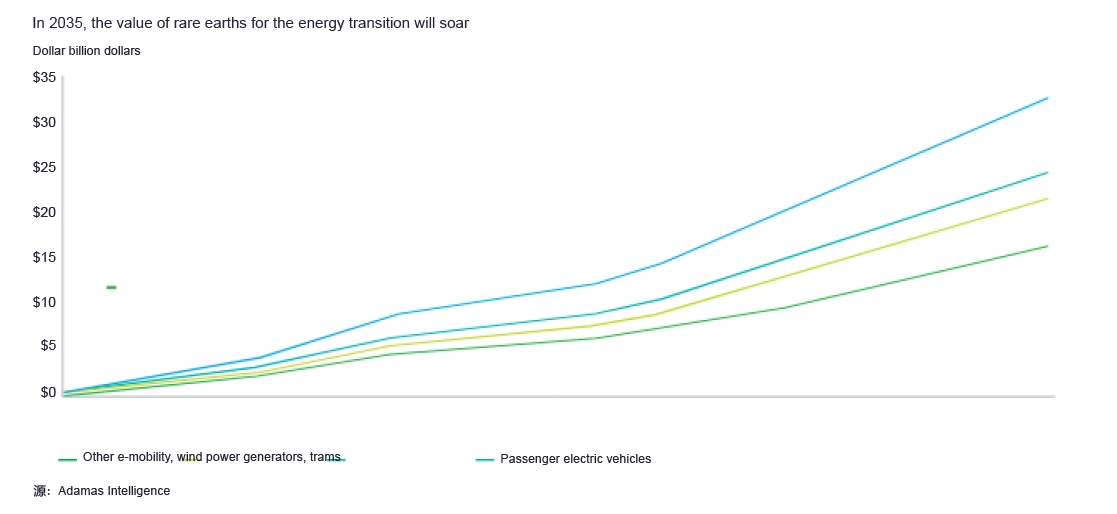

However, experts increasingly believe that meeting these targets will be extremely challenging. To achieve them, nations must accelerate deployment of renewable-energy technologies—such as wind turbines, solar photovoltaic panels, electric vehicles (EVs), and energy-storage systems. These technologies offer clear advantages in system efficiency and power quality, but their large-scale commercialization still faces significant technical and economic hurdles.

Rare earth elements are critical to enhancing the performance, size, and weight of electric vehicles. They play a central role in the manufacture of motors and generators: compared with conventional magnets, rare-earth-based permanent-magnet materials exhibit higher magnetic energy density and more reliable performance. This makes rare earths one of the key enabling foundations for driving the green revolution and realizing zero-emission goals.

Biometallurgy in which naturally occurring organic acids are used to extract rare earth elements. These bacterial acids are less efficient than hydrochloric acid and affect the commercialization of extraction.

Alternative materials are an alternative in which companies invest in R&D and adapt product designs to reduce or eliminate rare earth elements. Alternative technologies previously discussed, showing that manufacturers such as Tesla, Renault, and BMW are investing in alternative materials, but this may result in lower battery power, although cars driven primarily in cities may not need as long battery life. As continued technological advancements in the field, including magnetic alternatives, reliance on rare earth elements has driven R&D towards new avenues that could

Electric currents have been used to extract heavy rare earth elements such as dysprosium and terbium from ores. This reduces the amount of chemicals used, with less pollution but higher energy consumption.

Recommend

The supply of rare earths presents new and unique challenges that require coordinated efforts at the research, policy and industry levels to ensure a stable and sustainable supply of these vital resources. This will be achieved by: